If you’ve ever looked at your prescription receipt and wondered why one pill costs $5 and another costs $100, you’re not alone. The difference isn’t magic-it’s the tiered system insurance companies use to steer you toward cheaper drugs. In 2024, generic copays and brand copays still create wildly different out-of-pocket costs, even though both pills treat the same condition. Understanding how these tiers work can save you hundreds-or even thousands-of dollars a year.

How Copay Tiers Work in 2024

Most health plans, including Medicare Part D and private insurance, use a four-tier system to organize drugs by price. It’s simple: the cheaper the drug, the lower the copay. Here’s how it breaks down:- Tier 1: Preferred Generic - These are the cheapest options. Think generic versions of common meds like atorvastatin (Lipitor), metformin (Glucophage), or lisinopril (Zestril). Most plans charge $0 to $10 for a 30-day supply.

- Tier 2: Non-Preferred Generic - Still generic, but less commonly used or slightly more expensive. Copays range from $7 to $15.

- Tier 3: Preferred Brand - Brand-name drugs your plan encourages because they have better deals with manufacturers. Expect to pay $30 to $60.

- Tier 4: Non-Preferred Brand - Expensive brand-name drugs with no discount deal. Copays jump to $70-$120, sometimes higher.

Some plans add a Tier 5 for specialty drugs-like those for cancer, MS, or rheumatoid arthritis. Those can cost $150 or more per month, or even 33% of the total price.

Average 2024 Copay Numbers

Data from the Centers for Medicare & Medicaid Services (CMS) and the Kaiser Family Foundation (KFF) show clear patterns across Medicare and commercial plans:| Drug Type | Medicare Advantage (MA-PD) | Standalone PDP | Commercial Insurance |

|---|---|---|---|

| Preferred Generic | $4.50 | 22% coinsurance | 10-20% of cost |

| Non-Preferred Generic | $7 | 25-30% coinsurance | 15-25% of cost |

| Preferred Brand | $47 | 22% coinsurance | 30-40% of cost |

| Non-Preferred Brand | $100 | 47% coinsurance | 40-50% of cost |

Medicare Advantage plans usually charge fixed copays. Standalone Medicare Part D plans often use coinsurance-meaning you pay a percentage of the drug’s full price. That can be risky. If a brand-name drug costs $500, a 47% coinsurance means you pay $235. A fixed $100 copay is easier to budget.

Extra Help? Lower Copays for Low-Income Beneficiaries

If your income is limited, you might qualify for Medicare’s Extra Help program. In 2024, this program caps your copays at:- Generic drugs: $4.50 per prescription

- Brand-name drugs: $11.20 per prescription

That’s a huge difference from the $100+ some people pay without assistance. Even if you think you don’t qualify, it’s worth applying-many people miss out because they assume their income is too high.

Why Brand Drugs Cost So Much More

It’s not just about the pill. Brand-name drugs carry patent protection, marketing costs, and research fees. Generic drugs are copies. Once a patent expires, multiple companies can make the same drug. Competition drives prices down.But here’s the twist: sometimes, the generic isn’t cheaper at the pharmacy counter. A 2024 report from the Medicare Payment Advisory Commission (MedPAC) found that generic prices can vary wildly depending on the pharmacy, when you buy, and even the dosage form. One study showed a generic version of a common blood pressure pill costing $8 at Walmart but $24 at a chain pharmacy. Why? Some pharmacies are pressured by wholesalers to charge more for generics to keep favorable deals on brand-name drugs-a practice called “tying.”

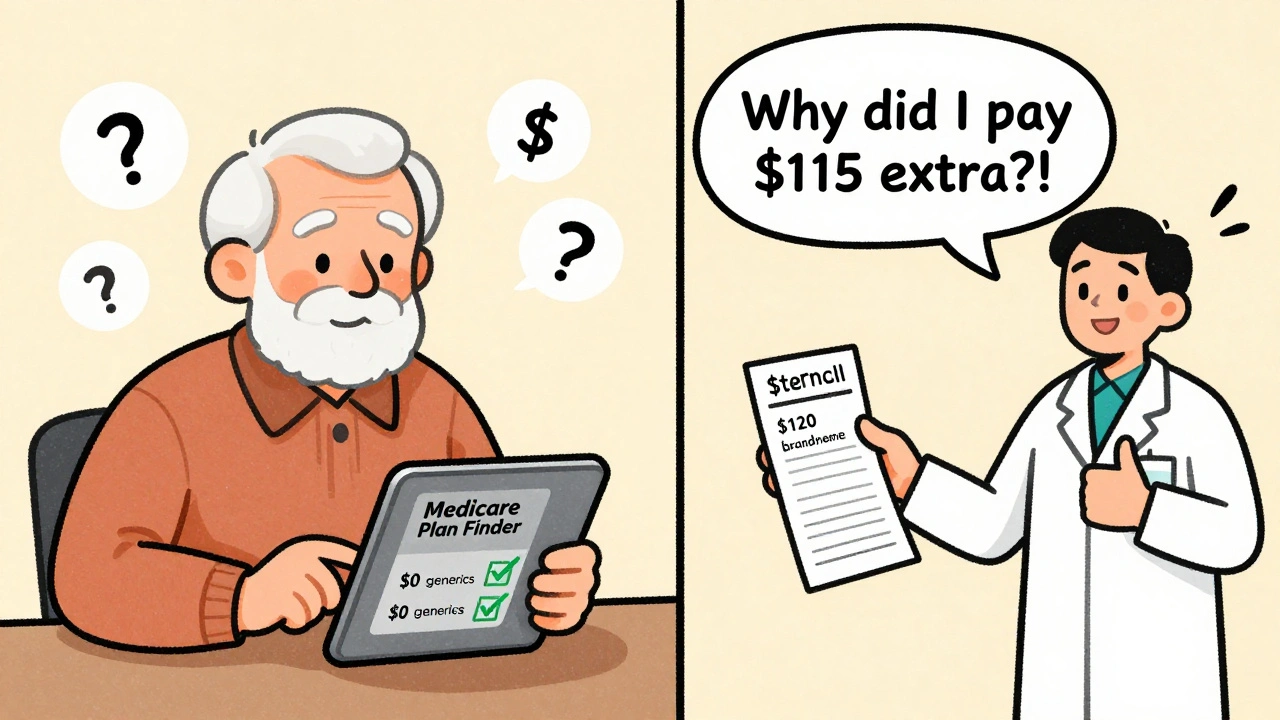

What Happens When You Choose a Brand Over a Generic

Some plans have a “Member Pay the Difference” rule. If your doctor prescribes a brand-name drug but a generic is available, you don’t just pay your normal copay-you pay the full price difference.Example: Your plan’s copay for atorvastatin (generic) is $5. Your doctor writes a prescription for Lipitor (brand). The brand costs $120. You pay your $5 generic copay, plus the $115 difference. Total: $120.

That’s not a mistake. It’s policy. And it catches people off guard. Reddit users and Medicare forums are full of stories like this: “I didn’t know I’d be charged $95 extra just because my doctor wrote ‘dispense as written.’”

How to Save Money in 2024

You don’t have to accept high copays. Here’s what actually works:- Check your plan’s formulary - Every year by October 15, your plan must publish a list of covered drugs and their tiers. Look up your meds. If your brand-name drug is on Tier 4, ask your doctor if there’s a preferred generic.

- Use the Medicare Plan Finder - Type in your exact medications, pharmacy, and zip code. It shows real prices across plans. A plan with $0 generics might cost more monthly, but if you take a brand drug, it could save you $800 a year.

- Ask about therapeutic alternatives - 72% of Medicare plans offer a cheaper generic or preferred brand that works just as well. Your doctor might not mention it unless you ask.

- Consider cash prices - Sometimes, paying out of pocket at Walmart or Costco is cheaper than your copay. Use GoodRx or SingleCare to compare. One user saved $67 on a 90-day supply of metformin by paying cash instead of using insurance.

- Get a plan review - If you take three or more meds, a free Medicare counselor can compare your options. Their audits show an average annual savings of $420.

What’s Changing in 2025

The Inflation Reduction Act is reshaping drug costs. Starting in 2025:- Out-of-pocket cap: You’ll pay no more than $2,000 a year for all your drugs, regardless of brand or generic.

- Insulin: Still capped at $35 per month.

- Generic copays: 98% of Medicare plans will offer $0 preferred generics.

This doesn’t mean generics will become free. It means your total drug spending is capped. If you take expensive brand-name drugs, you’ll save big. If you take mostly generics, your savings will be smaller-but still real.

Real Stories, Real Costs

A 72-year-old in Florida pays $95 a month for a non-preferred brand blood pressure med. The generic costs $15. Her doctor won’t switch her because of side effects. She’s stuck. That’s $1,140 a year just for one pill. Another man in Ohio switched from a $40 brand copay plan to one with $0 generics. He takes three generics and one brand. His annual drug cost dropped from $1,200 to $480.One survey found 63% of people using brand-name drugs struggled to afford them. Only 28% of generic users said the same.

Bottom Line

Generic copays are low because they’re meant to be the default. Brand copays are high because they’re meant to make you think twice. The system works-if you play by the rules.Don’t assume your plan’s copay is fair. Don’t assume your doctor knows your out-of-pocket cost. Don’t assume you’re stuck. Use the tools. Ask the questions. Compare the options. In 2024, the difference between a $5 generic and a $100 brand isn’t just about money-it’s about control over your health and your budget.

Why is my generic drug more expensive than the brand?

It’s rare, but it happens. Some pharmacies charge more for generics due to contracts with wholesalers, or because the generic is a different manufacturer that costs more. Always compare cash prices using apps like GoodRx. Sometimes paying cash is cheaper than using your insurance copay.

Can I switch from a brand to a generic without asking my doctor?

No. Your doctor must write the prescription. But you can ask your pharmacist if a generic is available and approved for substitution. Then, ask your doctor if switching is safe for you. Many conditions, like high blood pressure or cholesterol, respond equally well to generics.

Does Medicare Part D cover all generic drugs?

Not all. Every plan has a formulary-a list of covered drugs. Most cover at least two generics per category, but some may exclude certain ones. Always check your plan’s formulary before choosing a drug or plan.

What if my brand drug doesn’t have a generic yet?

You’ll pay the brand copay. But ask your doctor if there’s another brand drug on a lower tier that works just as well. Some plans have preferred brands that cost less than others. Also, manufacturers sometimes offer coupons or patient assistance programs.

Are generic drugs less effective than brand-name drugs?

No. The FDA requires generics to have the same active ingredient, strength, dosage form, and route of administration as the brand. They must also be bioequivalent-meaning they work the same way in your body. The only differences are inactive ingredients like fillers or dyes, which rarely affect how the drug works.

How do I find out what tier my drug is on?

Log into your plan’s website or call customer service. Every plan must provide a formulary list by October 15 each year. You can also use the Medicare Plan Finder tool, which shows drug tiers and estimated costs for each plan.

Jimmy Kärnfeldt

December 12, 2025 AT 10:39It’s wild how much power insurance companies have over something as basic as your health. I used to think generics were just ‘cheap knockoffs’ until I learned they’re literally the same chemistry, just without the marketing budget. Now I ask my pharmacist to swap anything I can. Saved me $800 last year just on blood pressure meds.

And yeah, the ‘member pay the difference’ thing? That’s a trap. My uncle got hit with $140 extra because his doctor didn’t check the formulary. He was furious. Nobody tells you this stuff until you’re already paying for it.

Ariel Nichole

December 13, 2025 AT 10:56Same here! I switched my diabetes med to generic last year and my copay dropped from $65 to $5. I almost cried. I didn’t even know I could ask for it - I just assumed my doctor’s prescription was set in stone. Turns out, you just gotta speak up. Also, GoodRx saved me on my inhaler - cash price was cheaper than my insurance copay. Mind blown.

Thanks for this breakdown. So many people are stuck paying way too much because they don’t know the system’s rigged.

john damon

December 14, 2025 AT 04:21bro why are we even paying for insurance if we still gotta pay $100 for a pill?? 😭💸

also i just paid $22 for a generic on goodrx and my insurance copay was $18 but i had to pay a $40 deductible so i literally lost money using insurance lmao

matthew dendle

December 15, 2025 AT 19:38generic drugs cost less because they dont have the fancy packaging or the celeb ads telling you to ask your doc about your blood pressure pill

also if your doc prescribes brand you're either rich or dumb

ps i paid 3 bucks for my generic lisinopril at walmart and my friend paid 120 for the same thing on insurance lmao

Taylor Dressler

December 17, 2025 AT 08:12One of the most important things people overlook is the formulary. Every year, plans change which drugs are on which tier. If you’re on a medication that’s been moved from Tier 1 to Tier 4, your out-of-pocket cost could jump overnight.

Don’t wait until you get the bill. Log into your plan’s portal every October during open enrollment. Use the Medicare Plan Finder. Even small changes - like switching from one generic manufacturer to another - can affect your price. And yes, cash prices are often better than copays, especially for common meds like metformin or atorvastatin.

Also, if your doctor says ‘no generic,’ ask why. Is it really medical necessity, or just habit? Most conditions respond identically to generics. The FDA doesn’t lie - they’re bioequivalent. If your doctor doesn’t know that, it’s time to find a new one.

Sylvia Frenzel

December 17, 2025 AT 08:49This whole system is a joke. Americans pay more for drugs than any other country and still get screwed. Why do we even have insurance if it doesn’t protect us from price gouging? I’m sick of being told to ‘shop around’ when I’m on a fixed income and can’t afford to waste time calling pharmacies.

Also, why do we have to rely on some website like GoodRx to get fair prices? This isn’t a free market - it’s a rigged casino.

Paul Dixon

December 17, 2025 AT 17:15Man I didn’t even know about the ‘pay the difference’ rule until my mom got hit with $110 extra last month. She’s 74, on Medicare, thought she was covered. She cried. I had to help her appeal it. Turns out the pharmacy didn’t even try to substitute the generic. They just charged her the brand price.

Now I check every prescription before she leaves the counter. If you’re not watching out for this stuff, you’re gonna get buried under bills. Seriously - ask questions. Even if you feel dumb. It’s worth it.

Monica Evan

December 18, 2025 AT 10:57okay so i had this moment last week where i was paying $47 for my cholesterol med and then i saw on goodrx it was $12 cash at cvs so i paid cash and saved $35 and now i feel like a genius 😅

also my pharmacist told me some generics are made in the same factory as the brand just with different packaging and labeling - so why are we paying 10x more??

ps i spelled copay wrong in my notes for 3 years and i still do it. sue me.

pps if you’re on meds long term - get a free counselor. they found me a plan that saved me $500 a year. zero hype. just straight help.

Jean Claude de La Ronde

December 18, 2025 AT 21:49Canada pays $5 for the same pills and we’re over here negotiating with pharmacies like we’re at a flea market. I swear, if you took the profit margins off brand drugs and gave them to the public, we’d all be swimming in cash.

Also, the fact that a $2 generic can cost $24 at one pharmacy and $8 at another? That’s not capitalism. That’s extortion with a pharmacy receipt.

And don’t even get me started on ‘preferred’ brands. Preferred by whom? The drug company’s sales rep, that’s who.

Jim Irish

December 19, 2025 AT 19:03The tier system is designed to reduce overall spending. It works if patients understand it.

Always verify the tier. Always compare cash prices. Always ask your pharmacist for substitution options.

Medicare Part D formularies are public. Use them.

Simple steps. Big savings.

Mia Kingsley

December 19, 2025 AT 20:08oh so now generics are better?? i had a generic for my anxiety med and i felt like a zombie for two weeks

my doctor said switch back to brand and i was human again

so your whole post is wrong

also i paid $10 for my brand and my neighbor paid $150 for the same thing so your data is fake

and why are you even talking about goodrx?? that’s for broke people

my insurance is premium so i dont need to care

also my cat takes better meds than your generic